Introduction

Imagine the following: A Chinese producer in Guangzhou is selling electronics to a customer in Rotterdam. The products are transported by truck to Shenzhen port, by sea to Europe, and over the rail to the Netherlands. Who pays for each leg? Who takes the risk in case of containers falling overboard in the middle of the ocean? At this point, CIP -Carriage and Insurance Paid To- comes in very handy. To importers who have to deal with multi-modal shipments, exporters who need to know the costs, and forwarders that have to manage client demands, learning CIP is no longer a choice, but a necessity. This article demystifies it all: what CIP is, how it is used differently than other shipping terms such as CIF and CPT, when it succeeds (and when it fails), what insurance requirements can confuse even a seasoned trader, and what strategies can be used in practice to prevent costly errors. Whether you are moving the consumer products between continents or raw materials using a complicated network of logistics, knowing how to use CIP may be the only difference between flawless operations and costly disputes freight and insurance costs.

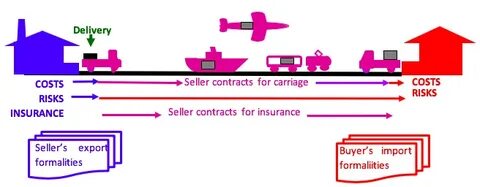

1. What Does “CIP” Mean in Shipping?

Carriage and Insurance Paid To (CIP) This is an Incoterm where the buyer and the seller agree to have goods shipped to a carrier, the seller meets the freight expenses, and the buyer is insured with minimum cargo insurance coverage benefits. But–and this is important–risk passes to the buyer as soon as goods are received by the first carrier and not when they are received by the destination freight costs.

As it is, it works in the following way: A Shanghai exporter sells machinery under the CIP Hamburg Incoterms 2020. The seller organizes and compensates the trucking to Shanghai port, ocean shipments to Hamburg and basic insurance to cover the whole trip. The liability to the delivery of the shipment is offloaded at the moment the freight forwarder takes the machinery in Shanghai parties involved. Any risk of loss or damage incurred by the buyer after this point is all borne by the buyer despite the seller covering the balance of the transport costs buyer’s country.

The essential seller duties consist of export clearance, delivery to the first carrier, freight payment to the named destination and minimum insurance (Institute Cargo Clauses C or equivalent 110% of invoice value under Incoterms 2020). The buyer does import clearance, destination unloading, and risk transfers on hand over. It is this division of costs (seller covers transport) and risk (buyer at risk early) that is so unusual about CIP and difficult to newcomers buyer’s premises.

2. How CIP Differs from Similar Incoterms

CIP vs CIF brings ceaseless confusion. Both involve the seller organising carriage and insurances to a specified location. The crucial difference? CIF is only applicable to sea and inland waterway transport, whereas CIP is applicable to any mode of transport air, road, rail, sea, or combinations. When you are shipping textiles using air, Hangzhou to New York, CIP would be suitable, but CIF would not. There are also differences in which under Incoterms 2020, CIP has an Institute Cargo Clause A coverage (extensive coverage) under the same requirements as CIF (minimal coverage). CIF is used in the case of traditional port to port sea freight, CIP is used in the case of containerized cargo transportation across various modes cip incoterms.

There is one difference between CIP vs CPT, and that is insurance. Carriage Paid To (CPT) is fully identical to CIP except that the seller is not required to have zero insurance. In CPT, the buyer has to provide his own coverage as soon as goods are out of the control of the seller. CIP is an inbuilt insurance, so it is more favorable when the customers do not possess insurance knowledge or desire an easy option. CPT is however more flexible and the buyer can tailor insurance to fit their specifications instead of taking the lowest coverage that the seller allots.

CIP vs DAP/DDP/EXW are more general comparisons. Under the Delivered at Place (DAP), early risk transfer takes place in CIP where the seller takes the risk to the end destination, unlike in Delivered at Place (DAP). DAP fits the consumer who does not want dealers to have all the logistics headaches. Delivered Duty Paid (DDP): The seller takes all the responsibility such as import duties and taxes. The other extreme is Ex Works (EXW) in which buyers will dictate and pay the whole journey since the sellers are not included in this process. CIP is somewhere in between: sellers are only in charge of transporting and rudimentary insurance, but the customers share the risk early and undertake the importation processes.

3. Pros & Cons of Using CIP

Seller benefits consist of known costs- they are charged at specific freight rates and negotiate transport at fixed costs with carriers. The issue of administrative convenience and insurance costs is also important; the experienced exporters usually know freight forwarders, and transport arrangements are effective. The early risk transfer covers sellers against claims relating to damage in the course of main carriage, as the buyers will own those risks once they have taken them initially.

Placing buyers do not have to organize complicated global logistics. The freight skills of the seller are usually able to negotiate better rates than those that individual buyers would be able to negotiate. Minimum insurance cover offers the lowest level of protection and does not even require buyers to raise a finger. To the buyers who are first time importers or those who deal with complex routing, CIP eliminates massive operational liabilities.

Risks and pitfalls also are a point of equal consideration. The sellers are under a risk in the event of goods being damaged before the delivery to the first carrier they are not insured against such accidents, which can happen even before the carriage has taken place. The buyers assume enormous risk just after handover and might not realize this. When a container ship goes under water, the buyer makes an insurance claim and also manages its aftermath, despite the shipping being paid by the seller, highlighting the buyer’s risk . The insurance cover provided by CIP is bare minimal; the insurer may buy the lowest policy that meets the legal requirements but is that is of low value or delicate items. Buyers that take extensive coverage when they are only facing basic cover have ugly surprises when claiming.

CIP is suitably advantageous in regular deliveries of medium-value items where both the involved parties are interested in equalizing the responsibilities. It is not as good when goods are unusually precious (and need airport bargaining), when there is need to have total control of the logistics, or when the sellers do not have trustworthy partnerships with carriers.

4. Insurance Requirements under CIP

Incentive Institute Cargo Clauses A with at least 110% coverage of the value of goods at the time of invoice is required by Incoterms 2020. This is a great deal better than earlier models. Institute Cargo Clause A is an all risk insurance coverage which insures against all loss or damage except certain exclusions such as inherent vice, ordinary leaks, or war risks (unless specified otherwise). The 110 percent includes the possible profit margins and other incidental costs.

Minimum cover is just what it is, minimum. The sellers meet their duty by buying basic ICC A policies. But 110 per cent of invoice value could be an enormous underestimation of the replacement costs, particularly when there is a variable exchange rate, price increment, or special equipment. A machinery invoice of $50,000 may attract to be covered with an amount of 75,000 when there is installation, loss of business, and the losses of profit by the time the replacement delays.

Further negotiation of insurance requires high-value or vulnerable cargo. The buyer must clearly state in the contracts: “Seller shall obtain a contract insuring [X amount] under Institute Cargo Clauses A [in addition to war androutes coverage]. Explain any special needs- refrigerated or shock-sensitive shipment of pharma, extended coverage of goods prone to theft. Do not think that the minimum insurance by the seller is enough.

The clauses to be monitored in the contract are insurance currency (must it be the same as invoice currency?), named beneficiary (is it supposed to be the buyer?), deductibles, exclusions, and claim procedures. Ensure that the insurance certificate has the right name of the buyer entity and the whole trip up to the destination mentioned. Certain policies either have geographic exceptions or seasonal restrictions. Ask insurers to provide copies of the insurance certificates prior to shipment of goods, and not when the troubles come about.

5. Practical Tips & Best Practices for CIP Shipments

Contract wording precision Precision in the wording of contracts eliminates conflicts. Specify: “CIP [precise site, e.g. 123 Industry Road, Frankfurt, Germany] Incoterms 2020.” These indefinite destinations such as CIP Germany confuse, there are thousands of delivery points in Germany and they all have varying cost. Specify the named place as much as possible: a terminal, an address of warehouse or a crossing of the border.

Seller’s checklist should include:arrange freight to named destination, take necessary minimum insurance (verify ICC A or equivalent), complete export customs clearance, deliver goods to first carrier with proper documentation, provide buyer with insurance certificate and transport documents, inform buyer of delivery of goods to carrier. Keep record of satisfying every obligation.

Buyer’s checklist: ensure that the insurance certificate is sufficient before shipment, clear import customs and pay duties/taxes, prepare receipt of the cargo at the named destination, realize that the risk passes to the first carrier when the shipment is received, track the shipment, claim insurance compensation directly in case of damage during carriage. Always wait to get home before realizing that there are gaps in the insurance.

Common pitfalls in risk management are to assume risk transfers at destination (it never does- it transfers at first carrier), to fail to review insurance facts until the loss has already taken place, to neglect to define unloading duties at destination and to misinterpret carrier paid as delivered safely. The other common mistake: sellers obtaining insurance that does not cover some types of transport, which are utilized during the trip.

Insurance negotiation pointers: In the case of valuable cargo, negotiate over 110. Add war risks, strikes coverage, and specific threats all risks endorsements should be considered. Talk valuation practices- agreed value policies do away with the controversy surrounding depreciation. In the case of serial shipments, consider open policies that deal with constant coverage and at lower rates.

Documentation tips: A bill of lading should indicate freight being prepaid, the seller should specify as the beneficiary and loss payee on the insurance certificates, the commercial invoices should have clear CIP terms and the packing lists should be detailed, and goods shipped to the buyer must be detailed to the customs and insurance. Keep records that show the seller supplied goods to the carrier in good condition- great in case of disputes of liability.

6. CIP Use Cases & Examples

Example 1: Electronics Shenzhen to Chicago: A Chinese producer sells tablets that have a value of 80 000 US dollars through CIP Chicago O’Hare International Airport. The seller ships the goods to Shenzhen airport (price 500), air-freights them to Chicago (price 6,200) and takes ICC A insurance of 88,000 coverage (price 450). Total seller cost: $87,150. Risk is transferred when the airline takes cargo in Shenzhen. Fifty tablets are ruined during flight due to rough handling. The customer makes claims against the policy that the seller took on the insurance. The customer also incurs Chicago import duties, customs broker fees, and final delivery to their warehouse costs (8000, 300, and 400).

Example 2: Multi-modal shipment of machinery: A German equipment manufacturer wants to ship machinery to Chongqing via CIP Chongqing Railway Terminal. The company ships via trucking to Hamburg port (€800), ocean transportation to Shanghai (€4,500), rail transportation Shanghai-Chongqing (€1,200), and ICC A insurance (€120,000) premium. The Chinese buyer invokes against the insurance when a crane drops the container in the exchange of container in the Shanghai port. Although the seller will have paid the rail leg up to Chongqing, the buyer will be the one who will suffer the damage.

Cost breakdown for $100,000 goods under CIP:

- Seller pays: export packing (1,500), local transportation (800), main carriage (8,500), insurance premium (600), export clearance (400) = 11,800 in total in addition to goods.

- Buyer pays: import duties (depending on country), clearance (customs) (300-800), destination offloading (200-1000), end delivery (depending)

- Risk transfers: First carrier, not destination.

7. When You Shouldn’t Use CIP

CIP should be avoided when the buyers require total control of logistics. Such huge retailers or well-established importers usually have contracted carrier rates that are better than those that sellers have access to. They like EXW or FCA, which gives them the chance to decide the route, the carriers, and the time. CIP makes them be part of the logistics decisions of the seller.

Goods of high value or very delicate nature render CIP risky unless highly adapted. Art, fine tools or drugs may need special transport, special insurance with no deductibles and controlled temperatures. The minimum insurance that the seller is required to provide under CIP is hardly ever enough, making additional insurance a consideration . Terms of DAP or DDP, in which holders of risk are the seller, are more likely to motivate cautious treatment.

CIP is problematic in some countries, as they have regulatory complications. There are countries where the importers must use local licensed insurers such that the foreign insurance certificate issued by the seller becomes useless. Some of them enforce complicated customs practices that are better served by local professionals recruited by the buyer. Know the country of research destinations before committing to CIP.

Risky routes or extreme weather are to be questioned. Minimum CIP insurance may not cover these perils in case of shipping through pirate infested waters, war zones or in cases where there is typhoon season. The buyers are to demand CPT (organizing their own comprehensive insurance) or to negotiate the improved insurance conditions that can be aimed at these risks.

Alternatives: FCA would be a better option when sellers desire to have logistics control at the earliest stage. During transit, the sellers should be motivated to take care of the product since sellers are able to take some risk up to final destination with the help of DAP. Use DDP to deliver turnkey in which the sellers are in charge of everything and even import compliance. CPT can be considered in the case when buyers, or buyer appointed party, possess better insurance schemes and do not wish to undergo basic coverage offered by the seller.

8. FAQs & Common Misconceptions about CIP

Is CIP governed by sea freight only? No. Compared to CIF (limited to the sea and inland waterway), CIP applies to all modes of transport: air, road, rail, sea, or combinations. This bi-directionality renders CIP excellent in contemporary containerized transportation which entails trucks, trains and vessels within one transportation run.

Who is the seller of the insurance and who is the buyer of the insurance? The seller is obligated to take insurance in the favor of the buyer. The seller pays premium but the beneficiary is the buyer who claims in case of goods damage during carriage. This is a difference in CIP and CPT where buyers take out their own insurance.

Does CIP have the requirement of full value insurance by the seller? Not necessarily in the full replacement meaning of the value. ICC A coverage of the incoterms 2020 involves 110 percent and above of the invoice value. This may not be the actual replacement costs, loss of profits or consequential damages. Sophisticated consumers will enter into more coverage than the bare minimum.

When is risk actually transferring under CIP? Risk is transferred when goods are shipped to the first carrier, and not at the named destination. This puzzles many individuals in that the seller pays the freight to the destination which makes one have the illusion that they have retained the danger in the long run. It is important to keep in mind that cost responsibility and risk transfer are different under CIP.

“Is it possible to use CIP in domestic deliveries? This will be technically yes, but rare. CIP normally regulates the international trade where export/import clearance, insurance and intricate logistics merit the structure of the term. Inland deliveries are usually made through less complex arrangements.

What happens when the goods received are damaged and the insurance will not cover it? The buyer suffers a loss when after the carrier handover, the damage happened and the insurance rightfully refuses the claim (exclusion applied, improper packing, etc.). This is a terrible truth that makes it harder to justify why consumers should ensure the sufficiency of insurance and the timing of risk transfer.

9. Conclusion

CIP provides a realistic compromise on international deliveries: suppliers can capitalise on their logistical knowledge, and ship to named destinations with a guaranteed freight, whereas buyers obtain a minimum of an insurance cover without organising complicated transportation. The key however is to realize that risk transfers with the first carrier and not at arrival and this is what leaves the unprepared traders in a dilemma. The insurance liability imposed on the seller is mandatory but offers minimum coverage which could be insufficient protection to the high value or sensitive cargo. Apply to regular multi-modes that both parties desire equal roles, yet negotiate better insurances on high-value goods and do not use at all when there is a requirement by the buyer to control the logistics of the shipment, or the risk is so high that it requires specialized coverage. ? Before signing any CIP contract, check insurance details, give specific destinations, clear up unloading duties and make sure that the parties know precisely when the risk passes. It does not matter whether you are transporting electronics to Asia, machinery to Europe or consumer goods across continents; knowing the specifics of CIP is a sure way to safeguard your own interests, including buyer’s responsibility, and avoid unnecessarily costly cross-cultural misunderstandings. You have time to compare incoterm options with your freight forwarder, get detailed quotes that break down costs and responsibilities and you must never assume that standard terms apply to your particular situation and the only difference is that you are getting the details correct in your bottom line.