Introduction: The Shipping Terms Dilemma

Suppose that you are importing electronics with a foreign supplier, and when you negotiate the contract, they give you two shipping options, which are CIF and CFR. The difference in price is $2,000- but what are you actually buying, including the freight cost, and more importantly what are you risking? To most businesses that are involved in international trade, the decision is a life and death issue as far as it comes to a smooth sail through a transaction and an expensive insurance gap in case something ails in the sea. The difference between CIF (Cost, Insurance, and Freight) and CFR (Cost and Freight) doesn’t simply concern terminology, but a way to protect your investment, liability, and to reduce costs in the supply chain. This all-inclusive guide will be dissecting these two Incoterms, contrasting their merits and limitations and assist you in determining which one suits better in your particular shipping circumstances.

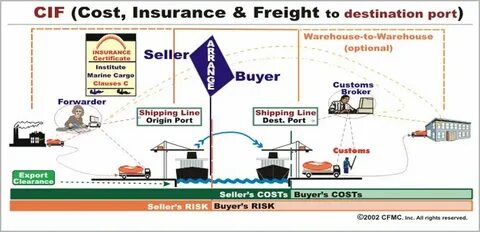

What Is CIF? (Cost, Insurance, and Freight)

The abbreviated CIF is actually Cost, Insurance and Freight, and it is also one of the most popular Incoterms in global maritime commerce. According to the CIF, the seller will bear all expenses involved in delivery of goods to the destination port- price of goods, freight, and most importantly marine cover. The seller should organize and insure cargo that will cover the cargo when it is in its ocean voyage. The term is only applied to sea transportation and inland waterway transportation as stipulated in the Incoterms 2020 regulations issued by the International Chamber of Commerce own additional insurance arrangements. The duties of the seller are to load the goods onto the ship, deal with the export custom clearance, freight costs to the ocean, and insurance to at least minimum coverage (usually Institute Cargo Clauses C or similar). It is worth noting, though, that though the seller covers these services and insurance costs , the risk is passed on to the buyer when the goods leave the rail of the ship at the port of origin.

What Is CFR? (Cost and Freight)

The CFR also known as Cost and Freight is the same thing that CIF is but with one exception: the seller does not include any insurance in their mandate. According to CFR, the seller bears goods cost, loading them to the vessel, clears them at the port of export and the freight transportation cost to the named port of destination. The seller is however not obliged to obtain insurance cover regarding the shipment. It implies that the buyer is not obligated to purchase insurance cover to protect the goods during transit, as the seller takes on the issue of the logistics and transportation.

Similar to CIF, CFR can only be applied to maritime and inland waterway transport by Incoterms 2020. Lack of compulsory insurance under CFR means that the buyers have greater freedom to select the levels of their cover and insurance companies, but it also puts the entire responsibility of risk management on them. The risk transfer point is the same as CIF- after goods are loaded onto the vessel at the loading port all risks of loss or damage are transferred to the buyer buyer assumes.

The Core Difference: Who Handles Insurance?

The main difference between CIF and CFR revolves completely around the issue of insurance responsibility. With CIF, the seller is required to take marine insurance and add this price to the contract price, issuing the buyer with an insurance certificate or policy as part of the shipping paperwork. In CFR, it is not required–insurance becomes the matter of the buyer, but the buyer is not under legal obligation to make a purchase. This distinction has great practical implications to both sides. With CIF seller insurance, the sellers usually use a minimum coverage to make the price competitive and the coverage may not offer full protection in high-value or high-risk cargo. Whenever buyers are issued with CIF shipments, they should closely examine the terms of insurance to make sure there is proper coverage seller’s responsibility. On the other hand, CFR purchasers may choose an all-inclusive insurance that fits their unique cargo and risk package, although it is up to them to ensure that they have it in place prior to shipment. This settlement does not just have an effect on cost allocation, it also affects liability exposure, claims process, and risk management approach in the entire supply chain.

Seller’s Responsibilities: CIF vs CFR

Within the CIF terms, the seller has obligations that are all inclusive and covers activities such as, transporting goods to the port of origin, packaging all the exportation formalities such as customs clearance and documentation, loading the cargo into the ship, paying ocean freight to the destination port, and acquiring the marine insurance with the lowest coverage. The seller has to furnish the buyer with a delivery evidence, commercial invoice, and an insurance certificate as part of the cost and freight cfr agreement . The liabilities of the seller are almost the same in CFR conditions, except that they do not need to arrange or pay insurance buyer’s inventory costs. The seller is yet to do the export clearance, deliver the merchandise to the ship, pay freight fees and also issue shipping documents such as the bill of loading and commercial invoice, but the insurance certificate has conspicuously been omitted. These two terms also mean that it must be the sellers covering all the expenses and risks until goods are loaded appropriately on the vessel upon shipment at the port. Subsequently, when the sellers are still paying freight on either terms, they cease being liable to loss or damage to the cargo on the ocean voyage.

Buyer’s Responsibilities: What You Need to Know

Bought under CIF and CFR, there are a few common obligations that are shared by the buyer. They have to clear importations on their own at the port of destination, pay all import duties, taxes and custom fees, and to provide land transportation between the port and the final destination. The buyer also adopts all the risks when the goods have been loaded into the vessel at the port of origin though they have not yet taken possession of the cargo physically shipping vessel

. The point of divergence between CIF and CFR is in the field of insurance management, where buyers may consider purchasing additional insurance . With CFR, buyers need to think strongly about buying their own cargo insurance because the seller has not given them any coverage- without any insurance the shipment is vulnerable to the potentially disastrous financial losses in the event of cargo damage, loss, or destruction at sea. When the seller has already provided basic insurance under CIF, the buyers may still desire to buy a supplemental cover when the policy of the seller has the minimum coverage. The smart customer will always read the insurance terms of CIF contracts and evaluate the need of extra coverage depending on the value of the cargo, risk in the route and their risk-taking capability purchase insurance coverage.

Cost Structure and Pricing Implications

The quoted price of CIF shipments is usually high compared to CFR shipments of the same supplier since the seller has included insurance premiums in the total price. Nevertheless, it does not always imply that CIF would be more expensive in general. The buyer should also assess the insurance premium provided by the seller, with the one that they would pay to receive similar coverage when making a purchase under CFR terms. In other instances, a buyer who has a relationship with the insurance companies or whose negotiating strength is much greater may get superior rates than that which sellers incorporate in the CIF prices. Also, there is the convenience factor, which is, it takes time, knowledge and administrative capabilities to deal with insurance arrangements which some shoppers do not wish to commit themselves to buyer’s costs begin. DF sellers can also spread a premium on the insurance part and so their overall price will be a little higher than a CFR quote plus a separate insurance. To make proper comparisons, buyers must demand separation of the insurance cost as a part of CIF quotes. The shipping frequency will also determine the price decision: companies that have frequent shipment volumes may be offered annual cargo insurance contracts at more advantageous rates, and CFR is more cost-effective in the long term.

Risk and Liability: Understanding Transfer Points

Another myth is that CIF has greater risk coverage than CFR, but this is not the case in terms of the timing to transfer risk. In both CIF and CFR, the buyer and seller trade off all risks at precisely the same point, which is when the goods are loaded on to the ship at the port of origin. Since then all the risks of loss, damage or destruction to the cargo are transferred to the buyer, whether the freight or insurance has been paid by that buyer or a different party buyer’s risk. The difference is what is in case something does go wrong on transit. In case of CIF the buyer may claim against the insurance policy issued by the seller, but there is a limit to such coverage and exclusions. In the CFR situation when the buyer did not provide insurance against the risk of cargo damage or loss at sea the buyer bears the entire financial loss unless the buyer can demonstrate negligence by the carrier and also succeed in a claim against the liability insurance of the carrier, which in most shipping arrangements is limited and therefore usually unsuccessful. This is extremely significant to insurance terms on CFR since purchasers would otherwise be subject to uncovered exposure to such risks hroughout the most risky stage of the trip.

Documentation Requirements for CIF and CFR

The shipments that take place in CIF and CFR require proper documentation, however, the names of the documents are somewhat different. Under CIF, the seller is required to deliver the buyer with commercial invoice of goods and their value, a bill of lading or sea waybill demonstrating that goods were loaded in the vessel, a delivery or shipping notice and insurance certificate or policy demonstrating that the cargo was insured and paid buyer pays. In CFR, the documentation requirement remains the same except the insurance certificate, which is not required despite the seller not having made an insurance cover. Buyers are to make sure that their purchase orders a clear description of who is supposed to be responsible to each document and the consequences in case of late or incomplete documentation. The insurance certificate of CIF is particularly worth special consideration–buyers must ensure that they are listed as the beneficiary, or that benefits can be assigned, the certificate must provide sufficient coverage, and must be in regard to all the risks to which their cargo and route are susceptible. There are clauses in the contracts, where all risks coverage is expected or a greater coverage than the minimum Incoterms coverage, which ought to be clearly written in the agreement.

CIF Advantages: When Seller-Arranged Insurance Makes Sense

CIF has some interesting benefits that especially apply to some sorts of buyers. First, it is convenient and easy to do- all logistics such as freight and insurance are taken care of by the seller thus lessening the administration load on the purchaser. This can be of particular benefit to small importers or those who are new to international trade and may not have the experience of negotiating with insurance companies or in knowing the terms of marine insurance. Second, CIF establishes one point of contact in shipping matters making the communication and problem solving easier. Third, insurance as part of the package removes the possibility that a customer would forget or put off the process of insuring or the cargo would not have insurance. Fourth, high-volume sellers usually have negotiated competitive shipping insurance rates which they can transfer, which is what makes CIF pricing appealing risk occurs. Lastly, CIF can help to simplify the customs clearance at the destination because all the documentation including insurance certificates is given collectively. CIF is an effective worry-free shipping option to buyers who place an emphasis on simplicity over control, or importers who are happy with minimum insurance coverage of the goods they are importing of moderate value.

CIF Disadvantages: Limitations and Concerns

CIF has some significant limitations that should be taken into account by buyers despite its convenience. The greatest weakness is that sellers usually purchase only the minimum insurance cover which is either Institute Cargo Clauses C or some other basic cover which does not cover a wide range of common risks and may not give sufficient cover to fragile or valuable goods. Buyers do not have or have little control over the choice of insurance company, the conditions of a particular policy or how claims are processed, which is how insurance costs affect their purchasing decisions . Also sellers can add mark up to the insurance premium, thus CIF is more costly than procuring individual coverage on CFR. The second issue is that there can be conflicts of interest: the insurer of a seller is unlikely to be interested in serving the interests of a buyer during settling claims icc’s tax payment. To very advanced consumers who have an existing insurance relationship or have a certain need of coverage, the one-size-fits-all strategy adopted by CIF may seem limiting. Lastly, when the goods are damaged, and the insurance of the seller is not sufficient, the buyer can have very little to claim, as they have trusted the insurance system of the seller instead of obtaining full coverage on their own.

CFR Advantages: Control and Flexibility

CFR has unique benefits that appeal to buyers that need more control over the management of their supply chain risks. The first advantage is the absolute freedom in the choice of the insurance coverage – the buyers are free to pick out the provider of their insurance, create terms of policies, define levels of insurance, and pick particular insurance that applies to the kinds of cargo and shipping route. This control is essential especially in the high-value freight cfr or where the goods are fragile or when the routes have high risk profiles where minimum insurance would not suffice. Customers who make frequent orders may also negotiate annual policies of marine cargo insurance at attractive terms and prices, and may do so at a better rate than sellers may use in CIF quotations. CFR also removes the insurance markup of the seller, and provides price transparency, the buyer can know the price they are really paying in insurance instead of the price being included in the overall cost. Also, direct work with an insurance company would create a connection that would streamline the process of claims and offer improved customer service should a problem occur. In the case of established importers who have good risk management skills, CFR offers the freedom of shielding their interest as they perceive it.

CFR Disadvantages: Risks and Responsibilities

The key drawback of CFR is that it leaves the insuring process to the buyer and the buyer needs to be active, informed and well-organised. Buyers who do not get insurance or underestimate insurance requirements face the risk of suffering incredibly huge losses should the cargo be ruined, lost, or destroyed during transit, so it is advisable for the buyer early to take action . This administrative task takes time, skills, and in certain situations access to specialized insurance brokers who understand marine cargo insurance. In small business or first time importers, it is too much to negotiate insurance cover and learn the language of the policies. Also, there is timing risk, where a buyer does not get to insure cargo and ships before the time expires to get insurance, which makes the goods travel without insurance. CFR also leads to fragmentation of service delivery whereby the acquisition buyer has to liaise solutions to the seller, freight forwarder and insurer instead of integrated service being offered under CIF. Lastly, certain consumers can just forget to take insurance and assume that the seller has done it, then they get some bad surprises when they finally claim. The responsibility that comes with the flexibility CFR offers is not something that every buyer can deal with.

How to Decide: CIF or CFR?

The decision between CIF and CFR needs to be made with a thorough consideration of various aspects particular to your business. Take into account the worth and delicacy of your cargo- high valued and delicate goods may require the thorough and customized cover that can be offered under CFR whereas normal merchandise may be sufficiently covered under the standardized coverage under CIF. Consider your level of experience and administration ability: in case you are a new importer or have a small team, the simplicity of CIF can be paid off any mark-up price. Criticize the relationship you have with your supplier and your confidence in their ability to deliver good service and remain reliable at least under CIF conditions may not call for such a term to be eliminated. Review how often you ship and the volume of your shipping: frequent importers can negotiate a yearly insurance policy regarding cfr and cif , which is more cost effective in the long run. Look at a particular shipping route and its risk profile- dangerous routes can need cover not just provided by sellers under CIF. Assess your risk tolerance and financial ability to take a loss–in case a complete loss of cargo to the ship would be devastating, it may be wise to have an all-inclusive insurance under CFR. Lastly, estimate real costs by getting CFR quotes and independent insurance estimates versus CIF quotes and insurance information, whereby, you can do an apples-to-apple comparison that takes both the price and the quality of the coverage into consideration.

Common Misconceptions About CIF and CFR

There are a number of common misconceptions regarding these Incoterms that can make it expensive to err. To begin with, most buyers are misled to think that under CIF the seller is the one who is at risk until goods reach the destination port merely because they paid freight and insurance- the reality is that in both CIF and CFR risk is transferred when the goods are loaded onto the ship at the origin. Second, a few of them suppose that CIF will always be more costly compared to CFR, nevertheless, when the price of independently arranged insurance and benefits of combined services are taken into consideration. Third, there is always a possibility that buyers may have a misconception that CIF insures the maximum coverage, yet in reality sellers will only offer minimum coverage that might not be adequate to cover high value cargo. Fourth, it is unclear who has to pay duties and taxes on imports – under both CIF and CFR, the buyer always has to pay. Fifth, certain traders would seek to apply CIF or CFR to air shipment or truck transportation, however, Incoterms 2020 clearly limits those terms to maritime and inland waters only. This knowledge will help businesses make informed decisions, based on the right information, not assumptions because such relationships can be quite expensive to misunderstand.

Conclusion

The choice between CIF and CFR should always be a matter of personal business needs, risk tolerance and the ability to run your business operations. CIF also provides convenience and ease as insurance is combined with freight and transportation costs, making it suitable when a small importer or with companies in need of a streamlined administration although the coverage might be simplistic. CFR gives flexibility and control giving buyers a chance to customize insurance to fit their specific needs and this is beneficial to experienced traders dealing with high-valued goods or those with previous experiences with insurance. Neither is always the best choice, and the answer is dependent on the value of the cargo, the frequency of shipping, dangers of routes, your level of expertise, and cost factors. Think carefully about your circumstances, compare overall cost including quality of insurance, and think whether it is more convenient to have the insurance handled by the seller or to have the flexibility of having your own cover. Knowing these significant distinctions and being frank with yourself and your abilities and priorities will allow you to pick the Incoterm that will protect your interests the most and streamline your international supply chain processes.