The Surprise That Cost $50,000

Sarah, a Texan who imports furniture, ordered a container of dining sets from Vietnam with CIF terms. The seller made her feel better by offering shipping and insurance. Three weeks later, her freight forwarder gave her bad news: the container had fallen overboard in rough water. The insurance company could only cover 70% of the loss, so she was still responsible for the other 50,000. But I guess CIF meant that the buyer is responsible until my port! She complained about the shipping terms.

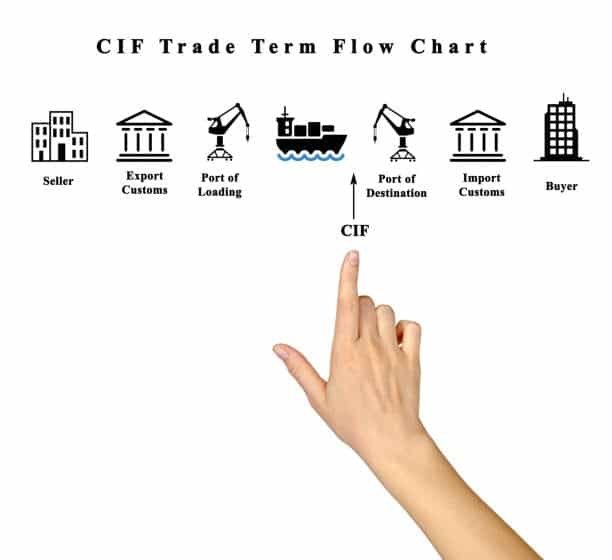

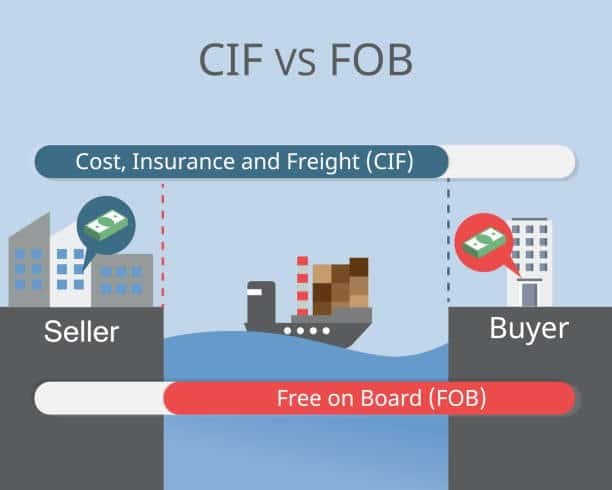

This situation shows one of the most misunderstood parts of CIF (Cost, Insurance, and Freight), which is one of the most misused trade terms in international business. An Incoterm for shipping by sea only, where the seller pays for the cost, insurance, and freight to the delivery port. But here’s the twist: As soon as the goods pass the rail of the ship at the loading port, the buyer takes on responsibility. This is known as the sea-loading risk point cif agreements.

Knowing how to split the CIF cost and risk can mean the difference between making money on imports and losing money.

Breaking Down CIF: The Three Pillars and Hidden Risk Transfer

CIF is built on three fundamental components, and each of these components has a unique set of burdens of obligation that come together to establish a unique risk-cost relationship in the context of the international business cif agreement.

The term “cost” refers to the sum of money that the seller is expected to pay in terms of all the transportation charges that might be incurred between their premises and the port of the buyer. The costs associated with inland freight, port handling, terminal charges, and document expenditures are included in this equation. For the purpose of constructing the first layer of the CIF cost vs risk split ultimate destination, these are the expenditures that are paid by the seller regardless of the date of the risk transfer.

In accordance with the insurance policy, the seller is obligated to cover and pay the minimum maritime cargo insurance, which is equal to 110% of the CIF value. Nevertheless, this coverage is subject to the basic insurance-at-sea regulation with Institute Cargo Clauses C, which is the most restrictive level and frequently results in an insurance claim being necessary. This basic criteria only takes into account the most significant dangers, including as fire, collision, and general average, as well as the possibility of theft, damage, or contamination being left behind, all of which have frequently been a problem for containerized shipments when goods arrives.

All of the expenditures associated with shipping from the loading port to the destination port, whether by sea or by interior waterways, are included in the pricing of freight. In addition, the seller is responsible for negotiating shipping arrangements, reserving cargo space, and receiving all payments and documentation related to freight.

The vulnerability is significant due to the fact that there is a risk transfer, in which sellers are responsible for all costs up until the point of destination, and purchasers are responsible for all risks after the risk point. This indicates that the buyer takes complete responsibility for the transaction. in order to go through the sea loading. This leads to a dangerous separation in which financial accountability and operational management do not coincide, which typically takes importers who are not well-versed in the subject by surprise.

CIF vs. Its Closest Cousins: Understanding the Critical Differences

As an international trader, you need to grasp the ins and outs of international commerce. Even little changes in international commercial terms can have a big impact on your bottom line. between comparable Incoterms that might make a big difference in your bottom line and have big benefits.

CFR (Cost & Freight) is like CIF (Cost & Freight) but doesn’t include the cost of insurance. The vendor has to pay for shipping to the target port, but the purchasers have to pay for their own shipping insurance. The risk transfer happens at the same spot as the CIF sea-loading risk, hence CFR is just CIF minus insurance. The choice is good when customers want to be in charge of their own insurance plans or get better rates on their own.

FOB (Free On Board) puts customers in a bad situation since they have to pay for everything and take on all the risk once the items have crossed the rail of the ship. FOB, on the other hand, creates congruence since the payer is the one who takes the risk, as stated in the sales contract. The purchasers are in charge of shipping and insurance, but they have to cope with intricate talks about freight and logistics.

CIP (Carriage & Insurance Paid To) covers all methods of transportation, not only maritime transport. However, it would need a more comprehensive insurance policy than CIF. CIP needs Institute Cargo Clauses A (all-risk protection), whereas CIF just needs Clause C (basic protection). This makes CIP better for high-value or fragile cargo that travels by container, truck, or plane.

CIP is especially useful when it comes to the insurance-at-sea rule for choosing containerized cargo transfers. This is because the items will transit through several points of handling and face many hazards of transfer that CIF’s minimal coverage is not anticipated to cover.

Strategic CIF Applications: When It Works and When It Backfires

CIF works well in some scenarios, such when commodities are being loaded into the ship. It might cause expensive problems if used in the improper shipping scenarios.

CIF is suitable for moving huge amounts of goods, such grains, minerals, or liquids, into ship holds without using containers. In these kinds of marketplaces, individual buyers typically don’t have a greater chance of getting better freight rates and insurance terms than professional sellers. CIF is very easy for novice importers because the sellers take care of the hard parts of shipping and packing for export. and the purchasers are in charge of growing the market.

Break-bulk goods CIF’s natural sweet spot is traditional break-bulk cargo, where the risk of sea-loading is in line with operations. It makes sense and is easy to manage to move the danger point when the bulk commodities are loaded under the ship’s holds. This is because the risk is minimal until they are discharged.

CIF gets complicated when the cargo is put in containers, which creates significant exposure gaps at the sea-loading risk point. The containers loaded at ports of origin can wait as long as days or weeks before the ship leaves. This puts buyers at risk of theft, damage, or port delays and possible import duties, especially when using inland waterways. Sellers, on the other hand, lose money and may not have any reason to speed up loading.

Under CIF conditions, electronics, fashion items, and other things that might go bad are at higher risk. Minimal insurance coverage seldom takes into account infection, temperature damage, or theft, which are common issues in container transit. FOB terms or arrangements are often more cost-effective for buyers who want more flexibility in their costs since sellers can charge more for freight and insurance services than they do for direct purchases.

Incoterms 2020: CIF’s Modern Framework

The recent revision of the Incoterms added strength to the old format of CIF and reflected on the modern shipping conditions and requirements on the insurance level.

CIF is still exclusively for maritime transit, however there is push to add other modes of transport. The International Chamber of Commerce kept this restriction in place and stressed that CIP has to be able to handle cargo that don’t come by sea and need more flexible transportation options.

Standards for insurance The present insurance rules still follow the Institute Cargo Clauses C, which only provide basic coverage. Most experts think this isn’t enough for today’s supply chains. Still, the Incoterms 2020 clearly lets purchasers and sellers agree on better insurance coverage, which means that parties must fix protection gaps by changing the contracts.

The change also made it necessary for sellers to provide insurance policies or certifications to buyers to show that coverage is at least at the minimal criteria. This kind of openness helps clients understand what they are at risk for and get more insurance if they need it.

The modern explanation shows that the sea-loading point of hazard is used to show how ships used to work, where after commodities were loaded, the ship owners were in charge of them. This notion works for bulk transportation, especially when products arrive at a certain port. However, it makes things more complicated for containerized freight, because loading and leaving might take a long time.

Real-World Case Study: Electronics Shipment Gone Wrong

For example, TechSource is an electronics store that buys smart phones in Shenzhen and ships them to Los Angeles. Their supplier has to arrange for ocean shipping and the least amount of marine insurance. They loaded the goods worth $200,000 into containers at Yantian Port.

The thieves broke into the container yard while the ships were waiting for three days to leave and stole $80,000 worth of goods. Techsource was at risk of losing money, even though the supplier was in charge of shipping, because the goods had already passed the point of risk for sea-loading when they were loaded.

TechSource lost $80,000 because the least amount of insurance they had against theft was when the goods were stored in port. They would have been better off getting full insurance against the risks of storing things at the port. Instead, CIP terms with all-risk insurance would have been safer.

This case demonstrates that CIF sellers can control shipping, but buyers must bear the risks, resulting in misaligned incentives; therefore, buyers must have direct access to risk management. That can cost a lot if there is a problem with the international shipping agreement.

Decision Checklist: Should You Use CIF?

Freight Experience: Do you want sellers to handle the shipping? CIF is a good choice for importers who don’t know much about shipping or don’t have a good relationship with freight companies. Still, more knowledgeable customers tend to think that FOB is cheaper and easier to handle than CIF insurance and freight.

What kind of cargo do you have? Bulk or break-bulk? CIF works very well with grains, minerals, and liquids because they go straight into the holds of ships. Containerized cargo is more likely to be at risk because the gaps in exposure are caused by the risk point that is seen as the sea-loading carriage paid.

Insurance Comfort: Are you okay with the least amount of coverage? CIF’s basic insurance may not cover cargo that is valuable or sensitive. Electronics, clothes, or food that goes bad may need better protection that is more in line with CIP or buyer-controlled insurance plans, which may include customs duty. freight by air.

Cost Control: Do you want to avoid having to negotiate a freight contract? CIF takes the buyer out of the shipping deal, but it usually adds costs for the seller. Customers who care about price often like the direct instruction of FOB on freight and insurance acquisition purchase insurance.

Risk Management: Can you handle the risks that come after loading? The CIF cost/risk split says that buyers should take on the risks of sea transport and sellers should choose how to ship things and get insurance. In some trade relationships, this lack of connection would be fine, but in others, it would be frustrating for people who want to find consistent incentives that the seller pays.

Conclusion

Cost, insurance, and freight are not the only components of CIF; rather, it is a complex risk-cost structure in which sellers are responsible for expenditures and purchasers are exposed to risks that extend beyond the sea-loading danger point. Importers are need to take into consideration both the opportunities and the traps that are presented by this fundamental distinction. CIF has a specific niche that is ideally suited for bulk items and novice importers who do not mind limited insurance coverage. This is in contrast to CFR insurance gap paying freight costs, FOB buyer control, or CIP enhanced coverage, which all have their own advantages. On the other hand, containerized shipments are typically exposed needlessly when CIF is used, which is why alternative Incoterms will be more appropriate. To properly implement CIF, it is necessary to take into account the fact that the cost of shipping is not the same as the risk of shipment; having this information may help save thousands of dollars in damages.